Deductible Health Insurance: A Comprehensive Guide

With the ever-increasing costs of healthcare, understanding the nuances of health insurance plans has never been more critical. One key component that often stands out in discussions about health insurance is the deductible. Here, we delve into the nuances of deductible health insurance plans, providing practical insights and real-world examples to clarify this often misunderstood aspect of health coverage.

Key Insights

- Primary insight with practical relevance: A deductible health insurance plan helps you manage out-of-pocket expenses by requiring you to pay a certain amount before insurance coverage kicks in.

- Technical consideration with clear application: Understanding how deductibles interact with copayments and out-of-pocket maximums can drastically impact your healthcare spending.

- Actionable recommendation: Always review the full terms of your health insurance plan to understand how deductibles affect your coverage and costs.

What is a Deductible?

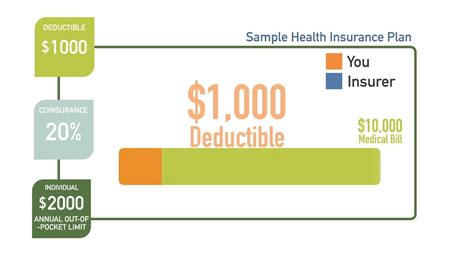

In the context of health insurance, a deductible is the amount you must pay out of pocket before your insurance begins to cover your medical expenses. Essentially, it acts as a threshold that your health plan uses to determine when benefits kick in. For example, if you have a 1,000 deductible and you visit a doctor for a minor illness, you will pay the full cost until you meet that 1,000 threshold. Once you meet the deductible, the insurance starts to cover a portion of your medical expenses, often through coinsurance.The Pros and Cons of High-Deductible Health Insurance Plans (HDHPs)

High-deductible health insurance plans, as their name suggests, have higher deductibles than standard plans. This can mean lower monthly premiums, which is attractive to many people seeking to reduce monthly healthcare expenses. For example, an HDHP may have a 5,000 deductible and a 100 monthly premium compared to a 500 deductible with a 300 monthly premium.However, HDHPs require policyholders to pay more before insurance benefits begin, which may be a concern for those expecting significant medical expenses. HDHPs often come with Health Savings Accounts (HSAs), which allow tax-advantaged savings for eligible medical expenses. This financial tool can be beneficial for those who manage their health well but might face substantial medical costs due to specific health conditions.

Strategies for Managing a Deductible Health Insurance Plan

Managing a plan with a high deductible requires strategic planning. First, it’s important to maintain good health to minimize medical expenses. Regular check-ups, preventive care, and a healthy lifestyle can substantially lower out-of-pocket costs. For those who anticipate significant medical needs, saving in a Health Savings Account (HSA) becomes crucial. HSAs allow you to save pre-tax dollars for qualified medical expenses, grow tax-free, and withdraw tax-free for eligible expenses once the deductible is met.Additionally, understanding your healthcare providers’ pricing and negotiating costs can further reduce out-of-pocket expenditures. Telemedicine services often provide a cost-effective alternative for minor health issues, helping you avoid higher costs associated with emergency rooms or urgent care facilities.

Can I use my HSA account to pay for my deductible?

No, you cannot use funds from your Health Savings Account (HSA) to pay your deductible. The HSA can only be used for qualified medical expenses after you meet your deductible for the year.

What happens if I don't meet my deductible?

If you don’t meet your deductible, your health insurance plan will not cover any medical expenses until you fulfill this requirement. For instance, if you have a $1,000 deductible and incur only $800 in medical expenses during the year, none of those costs will be covered by your insurance until the $1,000 is met.

In summary, a deductible health insurance plan is a crucial part of your overall health coverage strategy. By understanding how deductibles work and strategically managing healthcare costs, you can navigate this aspect of insurance more effectively.