Understanding the intricacies of the bond price formula is pivotal for financial professionals and investors alike. A bond is essentially a debt security representing a loan made to a borrower, typically a corporation or government. The bond price formula is central to determining the current value of a bond, enabling investors to assess the market value against its face value, and thus, make informed decisions. This comprehensive guide unpacks the bond price formula, elucidating the components and their interplay, with a focus on practical applications and real-world examples.

Key insights box:

Key Insights

- The bond price formula is foundational for evaluating a bond’s present value.

- Understanding the formula helps in discerning the impact of interest rates on bond valuation.

- Applying the formula enables investors to make strategic decisions based on market conditions.

In the financial world, the bond price formula is a critical tool for valuation. At its core, the formula calculates the present value of a series of future cash flows, which include periodic coupon payments and the redemption of the bond’s face value at maturity. This approach reflects the time value of money, an essential concept in finance, which dictates that a dollar today is worth more than a dollar in the future due to its potential earning capacity.

Components of the Bond Price Formula

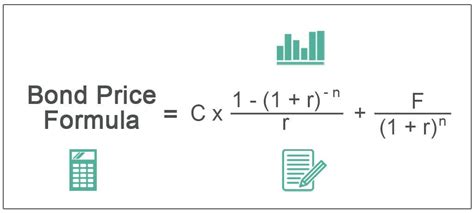

The formula for bond price, P, is expressed as follows:

P = C * [1 - (1 + y)^-n]/y] + F / (1 + y)^n

Where:

- C: Annual coupon payment

- F: Face value of the bond

- y: Yield to maturity (YTM) or discount rate

- n: Number of years until maturity

The first component of the formula is the present value of the coupon payments, calculated by discounting each periodic coupon payment to its present value using the yield to maturity. The second part calculates the present value of the face value, discounted by the same YTM.

Applications and Real-World Examples

Understanding the bond price formula is not merely academic; it has practical applications in real-world investment scenarios. For example, consider a bond with a face value of 1,000, an annual coupon payment of 100, and a yield to maturity of 5% that matures in 10 years. Using the formula:

P = 100 * [1 - (1 + 0.05)^-10]/0.05 + 1,000 / (1 + 0.05)^10

This calculation demonstrates how changes in interest rates affect bond prices. If market interest rates rise, the yield to maturity increases, leading to a decrease in the bond’s present value. Conversely, if rates fall, the bond’s price increases.

What is Yield to Maturity (YTM)?

Yield to maturity is the total return anticipated on a bond if held until it matures, considering all coupon payments and the redemption of the bond's face value. It reflects the annual rate of return that equates the present value of future cash flows from the bond with its current market price.

How does interest rate changes affect bond prices?

Interest rate changes have an inverse relationship with bond prices. When interest rates rise, the yield to maturity increases, decreasing bond prices. Conversely, when rates drop, the yield to maturity falls, increasing bond prices. This principle is crucial for bond investors to understand as it directly impacts portfolio valuations and returns.

This detailed exploration of the bond price formula elucidates its importance and practical utility in the financial markets. Armed with this knowledge, investors and financial professionals can more effectively navigate the complexities of bond valuation, making data-driven decisions to optimize their portfolios.