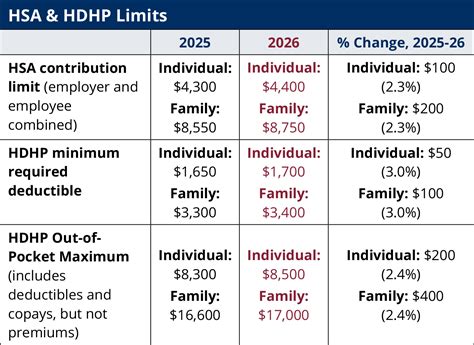

Understanding the Halifax Health Retirement Plan: A Strategic Guide for Employees

As employees of Halifax Health, navigating the retirement plan options is crucial for your long-term financial health. With a comprehensive range of benefits, the Halifax Health Retirement Plan offers not just a pathway to retirement but a significant financial cushion in your golden years. To maximize the benefits, understanding the plan’s intricacies is key.

Key insights box:

Key Insights

- Primary insight with practical relevance: Diversifying retirement investments can mitigate risks and optimize returns.

- Technical consideration with clear application: Understanding the vesting schedule is essential for maximizing employer contributions.

- Actionable recommendation: Regularly review your retirement plan portfolio to align with your financial goals.

A robust retirement plan provides not just security but peace of mind. The Halifax Health Retirement Plan is designed to offer various savings vehicles that cater to different risk tolerances and investment preferences. Employees can choose between traditional defined benefit plans, 403(b) tax-deferred annuities, and Roth IRA options. This flexibility enables individuals to craft a retirement strategy that best suits their unique financial situation.

In the early years of your career, it is crucial to understand the vesting schedule. The Halifax Health plan typically follows a 5-year cliff vesting method, meaning you must work for Halifax Health for five consecutive years to fully own the employer’s contributions. This period is critical, as it determines the extent to which you can benefit from employer matching contributions. For example, after the vesting period, you’re entitled to 100% ownership of employer contributions, significantly boosting your retirement savings.

As you progress in your career, it’s vital to diversify your retirement investments to mitigate risks and optimize returns. This means spreading your retirement savings across various asset classes such as equities, bonds, and real estate. For instance, investing a portion in low-risk bonds can provide stability, while allocating more to equities can capitalize on higher growth potential in the long run.

Maximizing Employer Contributions

One of the most compelling aspects of the Halifax Health Retirement Plan is the employer’s matching contributions. To make the most of this feature, employees should aim to contribute at least enough to receive the full match. This essentially means putting in money that effectively doubles the amount saved for retirement, without any additional effort.

For example, if Halifax Health matches 50% of your contributions up to 6% of your salary, contributing 6% of your salary directly translates to a 3% employer contribution. This is a no-brainer, as it’s essentially free money going into your retirement fund. It’s advisable to monitor and adjust contributions annually based on salary increments and financial goals.

Strategic Investment Choices

Strategic investment choices in the retirement plan can significantly influence the growth trajectory of your retirement fund. Halifax Health offers a range of investment options, each with varying risk levels and expected returns. Historically, diversified portfolios have performed better in the long run.

For instance, allocating 70% of your portfolio in equity funds and 30% in bond funds could be a balanced approach for someone nearing retirement. Equities tend to grow faster but are more volatile, whereas bonds provide more stability but lower returns. Regularly rebalancing your portfolio ensures it aligns with your risk tolerance and financial objectives as you age.

What happens if I leave Halifax Health before the vesting period?

If you leave Halifax Health before the vesting period, you may lose the employer contributions made on your behalf up to that point. It’s important to ensure you meet the vesting requirement to maximize employer contributions.

Can I contribute more than the maximum allowed by the IRS?

While you can contribute as much as you wish to your Halifax Health Retirement Plan, there are IRS-imposed limits on how much you can contribute annually. For 2023, the maximum contribution limit is 22,500 for individuals under 50 years old. Individuals aged 50 and above can make an additional catch-up contribution of 7,500.

In conclusion, the Halifax Health Retirement Plan is a powerful tool for ensuring a secure future. By understanding the vesting schedule, maximizing employer contributions, and making strategic investment choices, employees can build a robust retirement fund that supports their long-term financial goals. It’s not just about saving; it’s about smart saving tailored to your unique circumstances.